- 4 April 2023

- Posted by: Antonis Mouzakis

- Category: Tax News

The proof of awareness must be issued electronically at the request of the interested party and if this is not possible, then it is issued by any DOU or Control Center.

For which operations is the presentation of proof of awareness mandatory

a. For the collection of money or the repayment of payment instruments from the Public Sector, as long as the gross amount for each payment instrument exceeds €1,500, per beneficiary.

b. For the conclusion and renewal of loan, credit and financing contracts in general with the banks and other credit institutions recognized in Greece, as long as they are granted with the guarantee of the Greek State.

c. For the transfer of property due to encumbrance, parental provision, donation or voluntary auction, as well as for the voluntary creation of real estate rights, the distribution of joint real estate, the voluntary exchange of real estate and the creation of horizontal ownership.

d. To participate in tenders for the execution of public works or the provision of services or supplies by the Public Sector, as defined in the current legislation.

e. For the payment of the assigned monetary claims against the entities of case a. above.

f. For any other act, transaction or action for which proof of awareness is required by the provisions in force at any given time.

Exceptionally, proof of awareness is not required

a. From the Greek State, the State of other States, International Organizations, Local Self-Government Organizations, N.P.D.D.

b. From the receiver of the bankruptcy of a natural or legal person for acts or transactions concerning the bankruptcy estate, the liquidator of a company for the acts of liquidation, the guardian of the patrimonial inheritance, when acting proven for acts of liquidation of the patrimonial inheritance, as well as the liquidator of the inheritance for acts or transactions involving inheritance.

c. From permanent residents abroad, whether foreigners or expatriates, who were born abroad and retain Greek citizenship, as long as they do not earn income in Greece.

d. From the beneficiaries of the collection of fees or fixed remuneration in general from the provision of dependent work, pensions, alimony, expenses for the representation of public officials, hospital and funeral expenses, as long as the payment is made directly to the beneficiary employee, pensioner or his family or to a legally authorized person.

e. From the beneficiaries of insurance compensation and tort compensation, which are awarded by court decision.

f. For the establishment of a real right in favor of the State.

g. For beneficiaries of other non-confiscated monetary claims according to these provisions, as determined by the agency that carries out the liquidation.

h. It is not required to present evidence of awareness, if it is a distribution or exchange of joint real estate, establishment of horizontal or vertical ownership or modification of these without price, by the debtor who will acquire a real right on real property of a value at least equal to or greater than the value of the real right he had , as determined for the imposition of real estate transfer tax.

Conditions for granting proof of awareness are the following cumulatively

a. not to have total overdue basic debts of more than €30 certified to the Tax Administration. As long as there are total basic overdue debts above the aforementioned amount certified to the Tax Administration, the applicant must have settled them in a legal manner by suspending collection or by arranging partial payment, and

b. to have submitted the statements of the last five years, i.e. income tax statements, value added tax declarations and the periodic VAT declarations, which follow the last declaration and whose submission deadline has expired one month before the date of the application for the issuance of the proof of awareness.

c. In the cases where, during the audit, it is established that no declarations have been submitted for Wage Tax, Uniform Real Estate Tax, Real Property Tax .) and Real Estate Data of the last five years, an order to freeze the proof of awareness is registered in the TAXIS information system, which is lifted after the declarations have been submitted or when the relevant obligation no longer exists.

In particular, with regard to the above overdue debts:

a. For natural persons, individual debts are taken into account, as well as debts, for which the natural person is responsible for their payment, in accordance with the applicable provisions. For natural persons who are married, the personal debts of each spouse are taken into account separately and for wives, in addition, the debts certified in the name of their spouse, since according to the provisions in force they themselves are responsible for paying them.

b. For legal persons and legal entities, their debts are taken into account as well as the debts that have been ascertained against other persons and for which they are responsible for their payment, in accordance with the applicable tax and other provisions.

3. In order for a certificate of awareness to be granted, there must not be an order blocking the grant from another Authority.

4. In the case of the transfer of a property or the establishment of a real right over it without a price, no proof of awareness is granted, as long as the collection of the debt is not guaranteed. Exceptionally, in the event that the proof is requested for the distribution or exchange of joint real estate, the establishment of horizontal or vertical ownership or their modification, no security is required, if the debtor acquires a real right on real property of a value at least equal to the value of the real right he had, as determined for the imposition of real estate transfer tax. In the above cases, the corresponding notation will be written on the receipt.

Validity period of the proof of awareness

1. The validity of the proof of awareness is set at two (2) months, in the event that there are no certified debts.

2. The period of validity of the receipt is set at one (1) month, in case of non-overdue debts, debts that are suspended or have been subject to a partial payment adjustment program.

Application process - search - competent body

The proof of awareness must be issued electronically at the request of the interested party.

Type and content of the proof of awareness

1. The proof of awareness is a public document, it bears the title "PROOF OF AWARENESS FOR DEBT TO THE PUBLIC" and must contain the title of the issuing agency and the competent D.O.Y. of the taxpayer, the name of the natural person or the name of the legal person to whom it is granted, their address, the identity card number of the natural person, the Tax Registry Number, the date of issue of the receipt in writing, the serial number of the receipt, the purpose for on which it is issued, as well as the date of issue and its validity period in writing.

2. The proof of awareness also states:

a. the reason for its granting, as follows:

i) To collect money from Central Administration agencies.

ii) To collect money from public sector bodies (except Central Administration).

iii) For transfer of property.

iv) For any lawful use (except for collection of money and transfer of real estate).

b. In the proofs of monthly validity issued for the transfer of a property or establishment of a real right on it, the property to be transferred or on which a real right will be established with the property identification number (A.T.AK) if it exists.

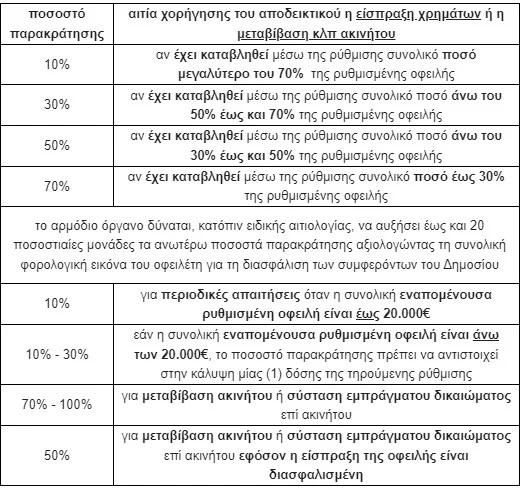

Withholding rate on proof of awareness

When a proof of awareness is issued for the collection of money or the transfer of a property or the creation of a real right thereon due to encumbrance and the taxpayer has debts that have been settled, in addition to the condition of the debtor's awareness of the partial payment arrangement, a condition of withholding part of the collected of claim, which is written on the receipt, as follows:

Especially in the event that the proof of awareness is granted for the transfer of a property or the creation of a real right over it due to a compelling reason and the overdue debts are not paid in full, a withholding percentage is set on the price, which is calculated on the real value of the property, but not at a value lower than the objective value.

* Antonis Mouzakis is a First Class Accountant - Tax Technician and Business Consultant in accounting and tax matters

Source: https://www.dnews.gr/eidhseis/oikonomia/443171/mouzakis-sto-dnews-perimenoume-ti-diataksi-gia-ti-forologisi-ton-airbnb https://www.dikaiologitika.gr/eidhseis/oikonomia/424341/gia-poies-prakseis-einai-ypoxreotiki-i-proskomisi-apodeiktikoy-forologikis-enimerotitas